KEY ARTICALE TAKEAWAYS

Fitch is helping securities issuers unlock the power of modern AVMs (automated valuation models). Fitch Ratings Inc. released a special report on September 27, 2019 updating residential mortgage-backed security (RMBS) criteria and disclosing their analysis of automated residential real estate valuations from multiple vendors. Fitch is a leading provider of credit ratings and research. The report, AVMs Can Play a Helpful Role in U.S. RMBS (paywall), lays out the risks and opportunities of using AVMs as alternatives to traditional valuation methods for second liens or seasoned performing loans and as a secondary value check for originations with full appraisal. Fitch’s description of how issuers can use AVMs in securitizations opens the doors for securities issuers to leverage advances in data-driven valuation products.

In an unprecedented move, the report includes the level of discount, or “haircut,” Fitch will assess in determining property valuation for reviewed vendors’ AVMs when used as primary valuations. Fitch also reports that they will accept reviewed vendors’ high-confidence AVMs as secondary valuations in due diligence, provided they are within 10% of a previously conducted appraisal.

By revealing this information about their risk assessment process, Fitch grants issuers and bond investors greater certainty. “Lenders use AVMs because they offer a fast, affordable, statistically derived estimate of a property’s value. Also, AVMs can provide more objectivity and are less susceptible to pressures to provide a specific value than appraisals performed by human appraisers, which could contain bias,” says Fitch.

Fitch determines their discount based on forecast standard deviation (FSD), a standard measure of confidence that HouseCanary routinely surfaces in our AVM tools. Fitch mapped each vendor’s internal measure of FSD to their accepted thresholds for each level of valuation haircut. Issuers can now combine this map with vendors’ hit rates at each FSD to determine the theoretical haircut Fitch will apply to values.

The Fitch report did not include information about the hit rate of each vendor. This is key information that issuers will need in order to understand the overall haircut and rating impact of their AVM choice. An AVM provider can easily increase its perception of accuracy by throttling hit rate and only submitting AVMs for data-rich properties in liquid, homogenous neighborhoods. Choosing an AVM that maximizes the coverage of your portfolio in each high-confidence band minimizes the haircut applied to the portfolio. It is therefore critical to ask your AVM vendors for their FSD levels on a given portfolio to fully utilize Fitch’s report.

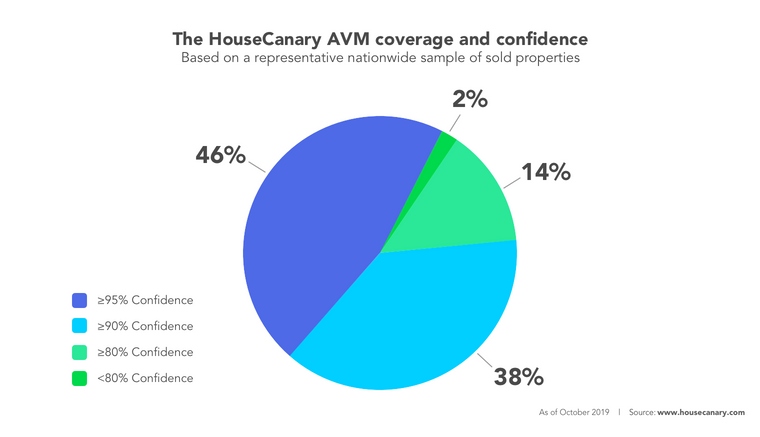

HouseCanary, for instance, has been shown by independent third party results to have among the highest hit rates of any AVM vendor. For additional context, we’ve broken down our confidence metrics based on our current hit rate for a representative nationwide sample of sold properties:

Users of a HouseCanary AVM product will see the minimum haircut (2.5%) on nearly half of a pool’s assets, resulting in a lower overall haircut compared to assets valued by non-reviewed vendors or AVMs with lower hit rates.

Based on performance testing of the HouseCanary AVM hit rate as of publication, 98% of all transacted properties that HouseCanary values would fall within Fitch’s 80% confidence threshold, meriting smaller haircuts. To illustrate what this means for lenders or investors valuing a portfolio of properties or liens, let’s look at an example of how an investor could use the HouseCanary AVM as the primary valuation for seasoned performing or second liens. The chart below shows the haircuts outlined by Fitch that would be applied to each FSD, or confidence level, threshold and the respective percentage of properties that would fall within each band in an unbiased, national level portfolio:

As of October 2019, 46% of HouseCanary AVMs typically fall within the ≤0.05 FSD band for an unbiased, national level portfolio of transacted properties. In a hypothetical $100 million portfolio consisting of 1,000 homes valued at $100,000 each, the total notional value of those homes would be $46 million. As we are a reviewed vendor, the haircut Fitch would apply to that portion of properties is 2.5%, resulting in a value of $44.9 million. The subsequent band of 90% confidence would be 38% (84%–46%) of the portfolio, or $38 million, which would receive a 5% haircut and result in a total notional value of $36.1 million. The discounting schema can be applied down the table for each threshold level. As shown, the overall, effective portfolio discount comes to 4.85%, resulting in a final post-haircut notional value of $95.2 million versus the $100 million initial valuation.

The HouseCanary AVM that Fitch reviewed so favorably is the same engine driving our onsite valuation products. Agile Evaluation is designed to fulfill the Interagency Guidelines (IAG) requirements for a qualified evaluation. According to the IAG, an evaluation must include a value conclusion and assessment of the actual physical condition of the property being evaluated. By providing a value conclusion informed by a physical inspection, Agile Evaluation aligns with these requirements. With Agile Evaluation, lenders get an evaluation report at a significant cost savings compared to a BPO or traditional evaluation, delivered in just a few days.

We have also paired the HouseCanary AVM with a third-party insurance partner to offer Agile Certified products. Agile Evaluation Certified is an evaluation designed to comply with IAG regulations, plus this product provides risk transfer coverage to the lender. Lenders can use Agile Evaluation Certified to expand their usage of evaluations within their existing risk guidelines.

HouseCanary’s hit rate continues to improve as we increase our brokerage coverage and analytics capabilities. Follow us on LinkedIn to stay posted on HouseCanary news and industry insights.

Frequently Asked Questions

No items found.

.png)